Banking is a risky business. The recent financial crisis of 2007/08 is still fresh in the minds of the Irish public but there is almost three centuries of banking failures in Ireland – some were unfortunate, while others were fraudulent. And like nowadays, some got away with their crimes, while others went bankrupt and some even went to jail.

There were other repercussions, for example, many of these banks issued their own banknotes and, after the bank closed, their banknotes were often worthless. Today, however, collectors pay large sums of money for some of these old, defunct and de-monetised banknotes.

- 1731 – The banking firm of Mead & Curtis (established 1710) in Dublin failed

- with debts of £10,500

- a relief Act was passed

- 1733 – Burton’s Bank crashed

- leaving debts of 79,128 pounds, 5 shillings and 4 pence

- 1754-55 – There was a major banking crisis when 3 banks failed due to frauds

- Dillon & Farrell Bank (bank collapsed in March 1754)

- Both partners absconded to France

- Willcox & Dawson Bank

- Lennox & French Bank

- Dillon & Farrell Bank (bank collapsed in March 1754)

- 1758 – Clements, Malone & Gore Bank failed

- 1759 – R. & T. Dawson Bank and Mitchell & Macarill Bank suspended payments

- this led to widespread panic and the remaining banks were government guaranteed

- 1779 – there was a further crisis, leading to failures of 2 banks

- Mitchell Bank

- Underwood Bank

In 1795 the Directors of the Bank of Ireland decided that credit would no longer be given for any private banker’s notes or drafts until payment in cash had been received by the Bank from the Bankers in question.

- 1797 – a run developed on banks in Dublin

In 1804, a new Act (44 Geo. III, c.91) declared all banknotes under 20 shillings invalid. This meant that all private banks issuing these small denomination notes had to find a way to withdraw them immediately. The obvious (and most common method) was:

- go into voluntary liquidation

- pay all creditors (note / bill holders) in full

- re-open with a different name

- issue larger denomination notes

The smaller, under-capitalised banks never recovered from the sudden run on their notes but, the more commercially astute, did.

1804 Malahide, Co Dublin – The Silver Bank, Three Shillings & Ninepence Halfpenny, payable in Notes of the Bank of Ireland. Six of these notes = One English Guinea.

- 1806 – Talbot & Co, also known as The Silver Bank (Malahide) – voluntary liquidation / all creditors were paid in full

- 1807 – Cotter & Kellet (Cork) – losses £210,000

- 1808 – Colclough & Co (New Ross) – note issue of £200,000 which became worthless

1802 Dublin, Beresfords Bank, contemporary forgery of Bank Post Bill for Three Guineas, 14 December 1802, stamped forgery

- 1810 – Beresfords Bank (Dublin) went into voluntary liquidation – all creditors paid in full and a new bank (Ball & Co) replaced it. Lord Beresford declared himself bankrupt and the other three directors went on to build a very successful business – until taken over by Northern Banking Co in 1888.

1814 (9 June) One Guinea Sterling ‘promissory’ bank note, underwritten by fFrench, Taaffe, Morris & Keeny. Note: Exchangeable for £1, 2s & 9d at the Bank of Ireland, in Dublin.

- 1814 – fFrench & Co (Tuam & Dublin)

- fFrench’s Bank was the largest and probably, the most infamous of the provincial private banks in Ireland. During the Napoleonic War the circulating money in Co Galway was almost exclusively country bankers’ notes

- Just two banks predominated

- – Lord fFrench & Co

- – Messrs. Joyce & Co

- Just two banks predominated

- Partners visited major fairs / markets in Co Galway exchanging their notes for Bank of Ireland notes

- Virtually all the bank notes in Connacht were Ffrench & Co notes by 1814

- It was often said that Ffrench’s banknotes were preferred to Bank of Ireland notes

- This was partially due to the fact that Ffrench’s notes were issued in Sterling (English pounds) which were worth more than Irish pounds

- Ffrench’s Bank notes were issued in the following nine denominations:

- £1; 1 guinea; 25 shillings; 30 shillings; £3; 3 guineas; £4; £10; and 10 guineas

- These banknotes were worth 8½% more than the equivalent Bank of Ireland notes

- Virtually all the bank notes in Connacht were Ffrench & Co notes by 1814

- Banknotes were not commonly used outside of the towns in Connacht

- Coins were is short supply and tickets (IOUs) replaced them

- These tickets were traded at a discount, multiple times – until a form of ‘bridging loan’ was required

- this resulted in ‘semi-legal’ usury and pawnbroking services (often at extortionate rates)

- this fictitious and objectionable currency enabled the people to carry on their business in the towns

- the Bank of Ireland intervened by issuing silver tokens (to the value of 5d, 10d and 6 shillings)

- the people, distrusting of coins in general and ignorant of their new silver content, stayed loyal to the ticket system and the extortionate usury / pawning

- On June 27th, the bank stopped payments and a commission of bankruptcy followed

- The bank had liabilities of £239,000 – £175,000 being in respect of issued banknotes

- The bank was owed £180,000 by its creditors but almost all of this was swallowed up by legal fees

- On December 9th, 1814, Lord Ffrench shot himself in the head (in a room in Trinity College Dublin, allegedly), in despair over the bank’s failure

- The collapse of Ffrench’s brought ruin to many in Co Galway

- Both landlords and tenants alike in the farming community

- Many business families also suffered

- The decline of several East Galway estates can be traced to the collapse of Ffrench’s Bank rather than the famine some thirty years later

- Most of the banknotes (over 50% of the £300,000 of banknotes in circulation) were never redeemed

- The collapse of Ffrench’s brought ruin to many in Co Galway

- fFrench’s Bank was the largest and probably, the most infamous of the provincial private banks in Ireland. During the Napoleonic War the circulating money in Co Galway was almost exclusively country bankers’ notes

- 1820 – major banking crisis in Munster

- All four banks in Cork closed from 25th May

- Within days, all four Limerick banks closed

- Closures followed in Clonmel (Riall & Co), Carrick-on-Suir, Kilkenny (Loughnane’s Bank), New Ross, and most spectacularly, Waterford

- Alexanders Bank closed in Dublin

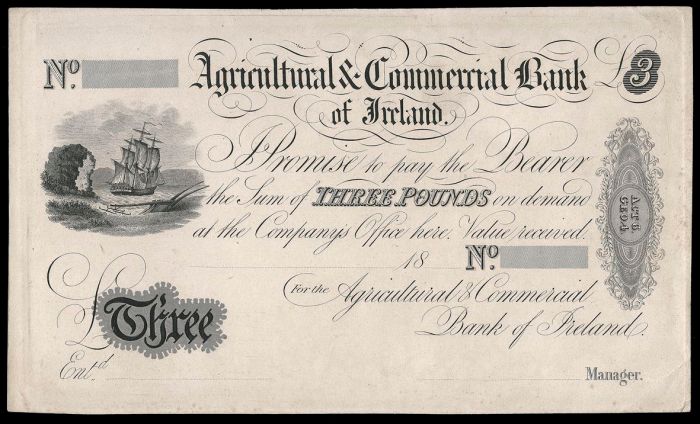

1811 Agricultural & Commercial Bank of Ireland, Three Pounds, 18___ , proof on light card

- 1836 – Agricultural & Commercial Bank failed

- The Agricultural & Commercial’s problems put all major banks under pressure

- The Bank of Ireland had to help out all joint-stock Irish banks to a total sum of £0.5 million

- Thomas Mooney’s bank was also allowed to fail

- 1856 – the Tipperary Bank failed

- Founded in the town of Tipperary in 1838 with a nominal capital of £0.5 million in shares of £50

- One brother, James Sadleir managed the bank

- The other brother, (John Sadleir, M.P.) dubbed The Prince of Swindlers (O’Shea, 1999) invested

- The bank was run fraudulently to fund his investment ventures and his gambling on the stock exchange

- John Sadleir committed suicide on Hampstead Heath on the night of 17-18 January 1856

- He was reincarnated as the villainous Merdle in Dickens’ Little Dorrit

- Glyn & Company, its London agents, refused its drafts on 9 or 10 February and provoked a run on its branches

- The Bank of Ireland tried to quell panic during the following week by buying up worthless Tipperary drafts

- The Tipperary Bank suspended payments in the following week and officially closed its doors a month after Sadleir’s death with liabilities of £430,000

- The problems of the Tipperary Bank forced La Touche’s Bank (an old private bank), the National Bank, and the Belfast Bank to seek help from the Bank of Ireland

- 1866 – Overend & Gurney Banks fails in London

- Bank of England decided that Overend & Gurney was beyond redemption

- The subsequent panic was alleviated via monetary easing

- The Overend Gurney crisis had ‘repercussions’ in Ireland

- La Touche’s Bank requested an overdraft of £50,000 of the Bank of Ireland

- The Royal Bank and the Hibernian Bank asked for £50,000 each, and the Munster Bank for £30,000

- The relatively small Union Bank of Ireland was a casualty; its branches were sold off to the Munster Bank and the Hibernian Bank before it went into voluntary liquidation

- The depositors got their money back eventually

- Shareholders who had been induced to part with more of their cash not long before the end—and at a time when the directors knew the writing was on the wall—lost everything

- 1885 – the Munster Bank failed

- The Munster Bank built up business partly by paying a generous return on deposits (as per Tipperary Bank)

- Its directors were involved in the Irish Nationalist Party (William Shaw was briefly its leader)

- Its activities prompted the bank of Ireland to expand into the smaller towns of Munster

- Insider lending brought down the Munster, i.e. the directors effectively looted their own bank

- These directors were declared bankrupt and not pursued via the courts

- The other shareholders and depositors lost everything

- When the Bank of Ireland refused to rescue it, a new bank (The Munster & Leinster Bank) was formed

- The Bank of Ireland (justifiably perceived as a ‘Unionist’ bank) was much criticized to failing to intervene

- This new bank closed its smallest branches and also closed branches in small towns with competition

- In the end £735,000 of its debts were written off,

- the bulk of which had been incurred in Cork (£306,000)

- and at the Dame St office (£266,000)

- This bank eventually emerged as the ‘lead bank’ in the formation of AIB in 1966