Introduction

To find something quickly on this long page, press the Ctrl key + F – a search box will appear on the bottom left of your screen. Type the word you are looking for and click on the down arrow (to go to that word).

The First Irish Banknotes

The first banknotes issued / used in Ireland were proto-banknotes issued by Dublin Goldmiths. This followed a pattern set by the Goldsmiths in London but the Wars of the Three Kingdoms, which ended with the Cromwellian invasion, destroyed the Irish economy and countryside. New towns and new industries would rise from the ashes.

Dublin would be re-built, re-imagined and re-invented. It would transform from a medieval city with 60,000 inhabitants to the ‘fourth most populous city’ in Europe (with 200,000 inhabitants) within a century. A mercantile class emerged in a city of wide streets, brick houses, industries and… private banks.

A re-construction of Dublin in 1610 (using Speed’s Map as a reference).

- 17th C Irish Banknotes (proto-banknotes)

- Joseph Demar, Dublin (1661)

- Considered to be the first Irish banker (money lender)

- Richard Hoare & Co, Dublin (1672-1694)

- A Goldsmith Banker that later became C. Hoare & Co (from 1688-94)

- Richard Hoare withdrew from the business in 1694 for political reasons

- Edward Hoare & Co, Cork (1672-1709)

- Joseph Demar, Dublin (1661)

The Earliest Banks in Ireland

In the charter first granted to the Bank of England in 1694; there was no prohibitory clause. But when the charter was renewed in 1708, it was enacted, that no other company formed of more than six persons should carry on the business of banking in England. This basic tenet was passed on to Scotland and, in turn, Ireland.

- Dublin (Burton & Falkiner) 1700-1733

- Dublin (Gardiner & Hill) 1700-1739

- Cork (Hoare, Joseph & Co) 1709-1740

-

1709

- Promissory notes were put on the same footing as inland bills of exchange.

- Notes issued by any “banker, goldsmith, merchant, or trader” whether payable to order or bearer, were rendered assignable and endorsible over as inland bills of exchange, and the endorsee might sustain an action thereon.

- James Southwell (Dublin) 17__ -1728

- Castle Street (died 1728

- Hugh Henry & Co (Dublin) 1710-1737

- Clonmell Bank (Riall, Phineas) 1715-1720

- Clonmell Bank (Bagwell & Co) 1720-54

- Clonmell Bank (Riall, William & Co) 1754-1820

- Two Guineas (Sterling)

- One Guinea (Sterling) – 1 Pound, 2 Shillings & 9 Pence (Irish)

- Six Shillings c. 1790

- Dublin (David Digges La Touche & Co) 1716-1879

- A private bank in Dublin and a gathering place for Huguenots who travelled outside Dublin, and left their money with him for security

- Customers were mainly aristocratic and professional

- The bank was taken over in 1879 by Munster Bank

- The bank was taken over in 1879 by Munster Bank

- James Mead & Co (Dublin) 1716-1727 – suspended payments with 10,500 of debtors

- Sir Alexander Cairns‘ Bank (Dublin) ?-1719

- Theobald Dillon & Co (Dublin) ?-1736 (thenceforth known as Thomas Dillon & Co

-

1720

1720 was the year of the infamous South Sea Bubble. In 1720, in return for a loan of £7 million to finance the war against France, the House of Lords passed the South Sea Bill, which allowed the South Sea Company a monopoly in trade with South America. The company underwrote the English National Debt, which stood at £30 million, on a promise of 5% interest from the Government.

- Shares immediately rose to 10 times their value

- 136 individual investors from Ireland holding £184,651 of stock lost their money

- These people were the third-biggest source of foreign investors in the South Sea Company

- Those figures, however, would have been dwarfed by the investments of Irish “wild geese” investors based in France who took positions in the South Sea Bubble.

- The country went wild, stocks increased in all these and other ‘dodgy’ schemes, and huge fortunes were made.

- Then the ‘bubble’ in London burst!

- The stocks crashed and people all over the country lost all of their money. Porters and ladies maids who had bought their own carriages became destitute almost overnight. The Clergy, Bishops and the Gentry lost their life savings; the whole country suffered a catastrophic loss of money and property.

- South Sea Company Directors were arrested and their estates forfeited.

- There were 462 members of the House of Commons and 112 Peers in the South Sea Company who were involved in the crash.

- Trust in bankers, banking and investment were at an all-time low

Despite this financial crisis, more private banks were formed that year

- Elnatan Lumm (Dublin) 1720

- A Goldsmith banker from Yorkshire

- Sir Abel Ram (Dublin) 1720

- A Goldsmith banker

-

1721

An attempt by wealthy landowners and merchants to form a National Bank of Ireland fails because MPs in the Irish Parliament feared that a national bank would overwhelm other businesses – especially if merchants were among its governors.

- Nuttall, Joseph & Co (Dublin) 1721-1738

- Swift, James & Co (Dublin) 1721-1746

- O’Brien Banknote Guide: James Swift & Co (Dublin) 1721-1746

- Early Irish Banknotes: 1713 ‘Sight Note’ (£28, 1s & 4d) James Swift

- O’Brien Banknote Guide: James Swift & Co (Dublin) 1721-1746

- Newcomen‘s Bank (Dublin) 1722-1825

- Customers were mainly aristocratic and professional

- The bank closed in 1825 following the death of its owner who reportedly committed suicide by shooting himself

- A creditors committee found the bank was managed ‘sovenly and wastefully’ with significant defalcations surrounding expenses related to family members

-

1724

In 1724, the bankers of Dublin issued a statement that they would not receive Woods’ halfpence as this would be detrimental to His Majesties Revenue and the trade of this kingdom. They were:

- Benjamin Burton & Francis Harrison (1700-1733)

- A former Dublin Goldsmith banker, who established a new banking business in 1700 at 4 Castle Street, along with a business partner, Francis Harrison.

- He died in 1728 and the bank became known as Samuel Burton & Co

- Hugh Henry & Ephraim Dawson (voluntary liquidation in 1737)

- James Swift & Co (taken over by Gleadowe & Co in 1746)

- Joseph Fade (1715-1748, thenceforth known as John Willcox & Co)

- Mead & Curtis (failed in 1727)

- David La Touche & Nathaniel Kane

- Richard & William Maguire

- Joseph Nuttall (failed in 1738)

-

1729

- Samuel Burton & Co (Dublin) 1728-1733

- Burton’s was one of Dublin’s largest and best known banks

- His father was a former Goldsmith banker, MP for Dublin and Lord Mayor

- They were bankers to the Irish Government and to Dublin Corporation

- This bank’s failure had serious repercussions through Ireland for decades to come and its affairs were not finally wound up until 1757. Many Acts were passed in order to prevent such a catastrophic failure.

-

1733 & 1735

- Samuel Burton and Daniel Falkiner

- Benjamin Burton, Samuel Burton and Daniel Falkiner

- Benjamin Burton and Francis Harrison

This bank carried on business in Dublin from the year 1700 to 1733. It was the leading early 18th C Dublin bank and, when Ben Burton died on 13 May 1728, the bank carried on but crashed in June 1733. The repercussions of this failure lasted for decades and a number of statutes were passed with reference to it, and then failed.

- In the interim, some of the early partners had purchased estates with the money deposited at the bank; and the Acts enabled the creditors to sell those estates

- The different names denote the changes which took place in the firm

Banking in 18th C Ireland became a high risk sector – especially for their creditors and something had to be done to improve standards. New laws were urgently needed. Nonetheless, new banks continued to appear in Ireland.

- Dublin (Thomas Dillon & Co) 1736-1754

- Took over from his father, Theobald Dillon in 1736

- Dublin (Mitchell, Henry & Co) 1739-1757

- Dublin (Richard Dawson & Co) 1740-1760

- Dublin (Lunell and Dickenson) 1742 – 1746 – failed due to financial panic after the Scottish Rebellion of 1745

- Dublin (James Dexter, Fleece Alley) 1745

- Dublin (Lunel & Dickson) 1745

- Dublin (Thomas Gleadowe & Co) 1746-1799

- Dublin (John Willcox & Co) 1748-1755

- Willcox took over from Joseph Fade in 1748 and re-named the bank)

- Cork (Lawton, Hugh & Co) 1750-1760

- Belfast (Mussenden, Daniel & Co) 1751-58

- Dublin (Lennox & French) 1751-1755

-

1754

The years following the Peace of Aix-la-Chappelle in 1748 saw a wave of unprecedented prosperity, and by the 1750s Dublin had eight banks. This boom ended in the major financial crisis of 1754-5, triggered by the failure of the Rotterdam correspondent of Dillon’s bank. There was a massive run on private (mercantile) banks in Ireland – only two banks survived, namely:

- La Touche Bank (David La Touche et al) 1700-1785

- Gleadowe & Co (Thomas) 1746-1799

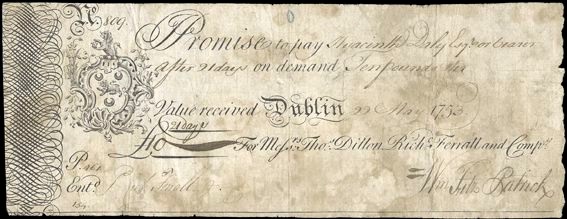

Most notorious was the collapse of Dillon & Ferrell in Dublin

- Dublin (Dillon & Co) 1736-54

- Richard Ferrall joined the partnership in 1748

- Traded as Dillon, Ferrall & Co (1748-54)

- The bank collapsed in March 1754

- Both partners absconded to France

- Traded as Dillon, Ferrall & Co (1748-54)

- Richard Ferrall joined the partnership in 1748

Dillon & Co, Ten Pounds, 22 May 1753, no. 809, for Thomas Dillon, Richard Ferrall and Co, signed by William Fitz Patrick.

Newly formed banks in 1754 included:

- Dublin (Thomas Finlay & Co) 1754-1829

-

1755

An Act passed to prevent bankers from trading as merchants, which would have given them an advantage in terms of issuing their notes. This move was prompted by the failure of most mercantile banks in 1754. Also: Partners of a bank were obliged to insert their names on every receipt (or note) issued by their bank.

- Cork Bank (Bayley Rogers & Co) 1755-1776

- Bayley Rogers, Boyle Travers & Henry Sheares (1755-1766)

- Bayley Rogers, Walter Travers & Henry Sheares (1766-1772)

- Bayley Rogers & Henry Sheares (1772-1776)

- Dublin Nathaniel Clements & Co) 1758 (failed within 4 months)

- Dublin (Malone, Antony & Co) 1758-1760

- Waterford (Newport‘s Bank) 1760-1820

- Cork Bank (Falkiner, Riggs & Co) 1760-1799

- Dawson, Coates, & Lawless (Dublin) 1763-1767

- Became Lawless & Coates Bank (Dublin) 1767-1793

- Dublin (Sir George Colebrooke & Co) 1764-1770

- A wealthy London banker who opened a branch in Dublin

- Dublin (Stewart, Sir Annesley & Co) 1765-1778

- Cork (Richard Tonson & Co) 1768-1773

- After the death of Tonson in 1773, it became known as Robert Warren & Co

- Cork (Pike, Ebenezer & Co) 1770-1785

- Cork Harper and Armstrong

- Traded directly with Portugal (Bills of Exchange)

- Also engaged in the Atlantic trade on a commission basis

- Wexford (Redmond’s Bank) 1770-1829 – failed & taken over by the Bank of Ireland

-

1771

-

1773

- Cork Bank (Robert Warren & Co) 1773-1784

- Collapsed in 1784 with debts exceeding £250,000

- Dublin (William Dunn) 1775

- Cork Bank (Walter Travers & Co) 1776-?

-

1777

- Cork (Hewitt, Williams & Co) 1776-1787

- Dublin (John Finlay & Co) 1778-1816

- Dublin (John Blake, Merchant) 1780-?

- Cork (Pike, Samuel & Co) 1785-1796

- The Limerick Bank (Maunsell‘s Bank) 1789-1820

Private Banks in Ireland during the Late 18th C

The Bank of Ireland was established in 1782 as a national bank but despite its massive resources and virtual monopoly it did not establish branches either within Dublin County or in the country towns.

- This gap was filled by an increasing number of small, private banks.

- These small banks were severely restricted via unlimited liability and not being allowed more than six partners

- There was a huge number of small private banks by the year 1800.

- Despite their numbers and their initial success, few managed to acquire sufficient capital to ensure stability

Their banknotes display a myriad of designs, denominations, signatures and placenames. As such, these early Irish banknotes provide students of notophily, economics, politics and history with a wealth of subject matter.

-

1785

Despite being the best capitalised bank in Ireland, with a virtual monopoly in Dublin, the Bank of Ireland did little to expand outside of Dublin, so small private banks continued to open in the provinces – especially in port cities and market towns.

- Cork (Roberts, Sir Thomas & Co) 1786-1815

- Belfast Bank (Ewing, John & Co) 1787-1796

- Belfast (Cunningham‘s Bank) 1789-1793

- Cork (Leslie‘s Bank) 1789-1826

- Belfast Discount Company (McIlveen, Gilbert & Co) 1793-1820

- Dublin (Ball‘s Bank) 1793-1888 – taken over in 1888 by The Northern Bank

- Dublin (Beresford‘s Bank)

- O’Brien Banknote Guide: Beresford’s Bank, Dublin 1794-1810

- Contemporary Forgery: (3 Guineas, Bank Post Bill, Beresford’s Bank)

- O’Brien Banknote Guide: Beresford’s Bank, Dublin 1794-1810

- Carrick-on-Suir (Sausse‘s Bank) 1794-1823

- Cork (Pike, Richard & Co) 1796-1800

- Belfast Bank (Hamilton, John & Co) 1796-97

- Dublin (Abraham Des Carrier & Co) 1797-1798

-

1797

On 27th February 1797, the Bank of England ceased to convert its deposit notes to gold specie in order to prevent a complete drain on its gold reserve. Initially the suspension of cash payments – the Suspension Period or the Bank Restriction Period as it became known – was intended as an emergency measure to ease panic following rumours of a French invasion. This led to the growth of small private banks, most of which issued their own notes.

The constant shortage of silver coinage in Ireland encouraged the widespread use of small notes, which were issued in varying denominations, by various merchants, businesses and private banks.

- The issue and usage of so-called tradesmens’ promissory notes was largely uncontrolled, and disapproved of by government, which sought to restrict them in an effort to control the perceived over-issue of paper money in Ireland.

The suspension of cash payments in 1797 exacerbated this, by prompting banks to increase their small note issues. There followed a rapid increase in note-issuing banks, closely followed by rapid iterations of banking laws to control them.

The Suspension Period was expected to continue only for a period of three weeks, or at most, until the end of the Napoleonic Wars. It remained in effect until 1st May 1821 and resulted in a huge amount of paper money being in circulation and an inevitable ‘adjustment’ at its end.

- Cork (Roche, Philip & Co) c. 1797

- Killarney (Murphy, William) 1797-

- O’Brien Banknote Guide: The Killarney Bank, Co Kerry 1797–

- Early Irish Banknotes: Three shillings & nine-pence ha’penny (3s 9½d)

- Early Irish Banknotes: Three British Shillings

- Early Irish Banknotes: One shilling & seven-pence ha’penny (1s 7½d)

- Early Irish Banknotes: One shilling & sixpence (1s 6d)

- Early Irish Banknotes: One shilling & a penny (1s 1d)

- Early Irish Banknotes: One British shilling

- Early Irish Banknotes: Nine-pence (9d)

- Early Irish Banknotes: Eight-pence ha’penny (8½d)

- Early Irish Banknotes: Sixpence Halfpenny

- Early Irish Banknotes: Four-pence (4d, or a groat)

- Early Irish Banknotes: Three-pence (3d)

- O’Brien Banknote Guide: The Killarney Bank, Co Kerry 1797–

-

1799

By the Act of 1799, banks within the City of Dublin were forbidden to issue notes for less than 5 guineas (£5 and 5 shillings). Banks outside this boundary were not subject to this restriction and, consequently, many new entrants to the banking sector chose rural Dublin villages outside of the canals to locate their businesses.

- Cork (Cotter & Kellett‘s Bank) 1799-1809

- Cork (Neweham‘s Bank) 1799-1824

- Cork (Roche, Stephen & Co) 1799-1820

- Dublin (Sir William Newcomen & Co) 1799-

- Dublin (Sir Thomas Lighton & Co) 1799-1805

- Became Robert Shaw & Co in 1805 when Lighton died

- Shaw’s Bank taken over by The Royal Bank of Ireland in 1836

- The Royal Bank, Provincial Bank, and Munster & Leinster bank merged to form Allied Irish Bank in 1966

- Dungarvan (Buckley, James & Co) 1799-?

- Enniscorthy (Woodcock‘s Bank) 1799-1804

- Early Irish Banknotes: Woodcock’s Bank, Enniscorthy – Six shillings

- Early Irish Banknotes: Woodcock’s Bank, Enniscorthy – Nine shillings

- Early Irish Banknotes: Woodcock’s Bank, Enniscorthy – Three Guineas (un-issued)

- Robert Woodcock’s Bank also issued coin tokens

- Minted by Küchler at the Soho mint in Birmingham, England

- Halfpenny Token, Type I (Enniscorthy Castle)

- Halfpenny Token, Type II (Woodcock crest & monogram)

- Minted by Küchler at the Soho mint in Birmingham, England

- Robert Woodcock’s Bank also issued coin tokens

- Enniscorthy (Codd, Clementine & Co) 1799-181_

- Enniscorthy (Sparrow, William & Co) 1799-180_

-

1800

- Athy (Mansergh & Co) 1800-

- Borris-in-Ossory Bank (partners unknown) 1800-

- Carnew (Blaney & Co) 1800-1803

- Clonmel (Watson, Solomon & Co) 1800-1809

- O’Brien Banknote Guide: Watson’s Bank, Clonmel (1800-1809)

- Six Guineas (Six Pounds, Sixteen Shillings & Sixpence)

- Half-Guinea (Eleven Shillings & Fourpence-halfpenny)

- Nine Shillings

- O’Brien Banknote Guide: Watson’s Bank, Clonmel (1800-1809)

- Cork (Newenham, George & Co) 1800-1824

- Cork (Pike, Joseph & Co) 1800-1826

- Cork (Roche‘s Bank) 1800-1820 – failed due to bad property loans when land prices fell

- Dungarvan (Fallon, James & Co) 1800

- Fermoy (Anderson, John & Co) 1800-1816

- Kilkenny (Loughnan‘s Bank) 1800-1820

- O’Brien Banknote Guide: Loughnan’s Bank, Kilkenny (1800-1820)

- Early Irish Banknotes: Loughnan’s Bank – Five Pounds Stg

- Early Irish Banknotes: Loughnan’s Bank – One Pound & Ten Shillings Stg

- Early Irish Banknotes: Loughnan’s Bank – One Pound Stg

- O’Brien Banknote Guide: Loughnan’s Bank, Kilkenny (1800-1820)

- Kilkenny (Williams & Finn) 1800-1806

- Kingscourt (Bank of Kings Court) 1800-

- O’Brien Banknote Guide: Bank of Kings Court, Co Cavan

- Early Irish Banknotes: Bank of Kings Court, Three Guineas

- Early Irish Banknotes: Bank of Kings Court,One Guinea

- O’Brien Banknote Guide: Bank of Kings Court, Co Cavan

- Youghal Bank (George & Richard Giles) 1800-1810

-

1801

- Birr (Bernard, Thomas & Co) 1801-1812

- Castlebar (Carr & Co) 1801

- Callan (Hearn, Michael) 1801-1807

- Early Irish Banknotes: Callan Bank – Three shillings & nine-pence ha’penny

- Early Irish Banknotes: Callan Bank – One Shilling & One Penny

- Cork (Delacour‘s Bank) 1801-1835

- Dublin (McMullen, John & Co) 1801-1802

- Killarney (Deanagh Mills) 1801-

- Early Irish Banknotes: One pound, two shillings & ninepence (One Guinea)

- Limerick (Roche’s Bank) 1801-1825 – acquired by the Provincial Bank of Ireland

- Waterford (O’Neill‘s Bank) 1801

- Early Irish Banknotes: Six Shillings

-

1802

- Dungarvan (Barron & Co) 1802-1803

- Galway Bank (John Joyce & Francis Blake) 1802-1813

- Early Irish Banknotes: The Galway Bank, 30 Shillings

- Early Irish Banknotes: The Galway Bank, 25 Shillings

- Early Irish Banknotes: The Galway Bank, 1 Pound, 2 Shillings & 9 Pence

- Early Irish Banknotes: The Galway Bank, 6 Shillings (Silver Note)

- Early Irish Banknotes: The Galway Bank, Three Guineas (Post Bill)

-

1803

- Carlow (Bennett, John & Co) 1803-

- Charleville (Evans, Eyre & Co) 1803-1805

- Enniscorthy (Redmond, Richard & Co) 1803-1815

- Malahide Bank (Talbot & Co) 1803-1804 – renamed Malahide Silver Bank in 1804

- Early Irish Banknotes: Malahide Bank, 9 shillings

- Tipperary (Scully‘s Bank) 1803-1838 – taken over by the Tipperary Bank

-

1804

In 1804, a new Act (44 Geo. III, c.91) declared all banknotes under 20 shillings invalid. This meant that all private banks issuing these small denomination notes had to find a way to withdraw them immediately. The obvious (and most common method) was:

- go into voluntary liquidation

- pay all creditors (note / bill holders) in full

- re-open with a different name (if still solvent, with an appetite for business)

- issue larger denomination notes

The smaller, under-capitalised banks never recovered from the sudden run on their notes but, the more commercially astute, did manage to find a way. Nevertheless, these small banks were vulnerable in a period of economic change and most of those remaining failed in the ‘deflation and depression’ period after the end of the Napoleonic Wars in 1815.

- Athy (Rawson, J.T. & Co) 1804-06

- Aughnacloy (Falls, James) 1804

- Ballinakill (Goss, Anthony) 1804-07

- Ballinakill (Savage, Michael) 1804

- Belfast (Malcolmson‘s Bank) 1804-1820

- Bray (The Silver Bank) 1804

- Early Irish Banknotes: The Silver Bank, Bray – 6 Shillings & 9½ Pence

- Carrick-on-Suir (Sausse, Richard & Co) 1804-1824

- Dublin (Thomas Knox Hannyngton) 1804-1816

- Dublin (Rose, Alderman John) 1804

- Dublin (Williams & Finn) 1804-1806

- Irish Banknote Guide: Williams & Finn (Kilkenny & Dublin) 1804-1806 due soon

- Early Irish Banknotes: Kilkenny Bank – 1½ Guineas (Sterling)

- Early Irish Banknotes: Kilkenny Bank – 1 Guinea (Sterling)

- Early Irish Banknotes: Kilkenny Bank – 1 Pound

- Irish Banknote Guide: Williams & Finn (Kilkenny & Dublin) 1804-1806 due soon

- Drogheda Bank (Hughes)

- Early Irish Banknotes: Drogheda Bank – Six Shillings (1804)

- Dungannon (Thomas Knox Hannyngton) 1804-1816

- Ennis (McMahon, Francis & Co) 1804-1808

- Killarney (Ross Island Mining Company) 1804-1819

- Irish Banknote Guide: Ross Island Mine (1804-1819)

- Early Irish Banknotes: Six Shillings & Sixpence (1804-1810)

- Early Irish Banknotes: Three Guineas (1812-1819)

- Irish Banknote Guide: Ross Island Mine (1804-1819)

- Kinsale (Kinsale Corporation) 1804

- Early Irish Banknotes: Kinsale, Threepence Halfpenny

- Early Irish Banknotes: Kinsale, Threepence

- Longford Bank (Fleming & Cunningham-Gouldsbury) 1804-1808

- Early Irish Banknotes: The Longford Bank, One Guinea

- Early Irish Banknotes: The Longford Bank, Four Guineas (Post Bill)

- Malahide Silver Bank (Talbot & Co) 1803-1804

- Early Irish Banknotes: The Silver Bank, 3 shillings & nine-pence ha’penny

- Early Irish Banknotes: The Silver Bank, 6 shillings

- Tuam (Ffrench‘s Bank)

1805

- Charleville & Limerick (Bruce, George Evans & Co) 1805-1820

- Dublin (McCreerey, Alexander & Co) c. 1805

- Dublin (Shaw‘s Bank) 1805-1836 – taken over by The Royal Bank of Ireland in 1836

- The Royal Bank, Provincial Bank, and Munster & Leinster bank merged to form Allied Irish Bank in 1966

- Galway (Lynch, Mark & Co) 1805-1814

1806

- Carrick-on-Suir (Carshore, Joseph & Co) 1806-1809

1807

- Dublin (Henry Alexander & John Bond) 1807-1808

- Dublin (Ffrench‘s Bank) 1807-1812 – a branch of Ffrench’s Tuam Bank

- Hon Sir Charles Ffrench, Michael Morris, William Keary, Charles Ffrench

- One Hundred Pounds (printed but unissued).

- This is the highest recorded denomination for a private bank in Ireland.

- There is a specimen in the National Museum of Ireland

- Ten Pounds (printed but unissued)

- One Pound, Ten Shillings

- Thirty Shillings

- One Pound, Five Shillings

- One Hundred Pounds (printed but unissued).

- Hon Sir Charles Ffrench, Michael Morris, William Keary, Charles Ffrench

1808

- Belfast Bank (Gordon, David & Co) 1808-25 – changed its name to Batt’s Bank in 1826

- Limerick (Bruce‘s Bank) 1808-1820

1809

- Belfast (Malcolmson‘s Bank) 1809-1820

- Belfast (Montgomery Bank) 1809-1824 – taken over by the Northern Bank in 1824

- Belfast (Tennant‘s Bank) 1809-1827 – merged with Batt’s Bank in 1827

1810

- Ennis (John O’Donnell) 181_ -?

- Early Irish Banknotes: One Guinea

- Ennis (Michael O’Brien / Ennis Mills) 181_ -?

- Early Irish Banknotes: One Guinea

- Dublin (Sir William Alexander & Co) 1810-1820 – failed with heavy losses

- O’Brien Banknote Guide: Sir William Alexander’s Bank (Dublin) 1810-1820

- Type A – Sir William Alexander & Robert Alexander Jnr. (1810-1811)

- Early Irish Banknotes: Alexander’s Bank (Type A) One Pound

- Type B – Sir William Alexander, Robert Alexander Jnr., William James Alexander & William John Alexander (1811-1818)

- Early Irish Banknotes: Alexander’s Bank (Type B) Thirty Shillings

- Early Irish Banknotes: Alexander’s Bank (Type B) Twenty Five Shillings

- Early Irish Banknotes: Alexander’s Bank (Type B) One Pound

- Type C – Sir William Alexander, Robert Alexander Jnr., William James Alexander, William John Alexander & William John Alexander Jnr. (1818-1820)

- Early Irish Banknotes: Alexander’s Bank (Type C) Five Pounds

- Early Irish Banknotes: Alexander’s Bank (Type C) Four Pounds

- Early Irish Banknotes: Alexander’s Bank (Type C) Three Pounds

- Early Irish Banknotes: Alexander’s Bank (Type C) Two Pounds

- Early Irish Banknotes: Alexander’s Bank (Type C) Thirty Shillings

- Early Irish Banknotes: Alexander’s Bank (Type C) 1½ Guineas

- Type C (Post Bills)

- Early Irish Banknotes: Alexander’s Bank (Post Bill) Five Pounds

- Early Irish Banknotes: Alexander’s Bank (Post Bill) Four Pounds

- Early Irish Banknotes: Alexander’s Bank (Post Bill) Three Pounds

- Type A – Sir William Alexander & Robert Alexander Jnr. (1810-1811)

- O’Brien Banknote Guide: Sir William Alexander’s Bank (Dublin) 1810-1820

- Dublin (Benjamin Ball & Co) 1810-1888

- Dublin (Stewart, Sir John & Co) 1811

- Cork (Morris, Abraham & Co) 1812-1815

- Dublin (Ffrench, Charles & Co) 1812-1814

- Infamous Irish Banks: Lord ffrench & Co (Tuam & Dublin) 1812-1814

- Type A – Charles FFrench, Michael Morris & William Keary (1812 only)

- ?

- Type B – Charles FFrench, Henry Taaffe, Michael Morris, William Keary & Thomas FFrench (1812 only)

- Early Irish Banknotes: Ffrench’s Bank (Dublin) One Guinea

- Type C – Charles FFrench, Henry Taaffe, Michael Morris, William Keary, Thomas FFrench & Martin FFrench (1812-1814)

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Ten Pounds

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Four Pounds

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Three Guineas

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Three Pounds

- Early Irish Banknotes: Ffrench’s Bank (Dublin) 1½ Guineas

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Thirty Shillings

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Twenty Five Shillings

- Early Irish Banknotes: Ffrench’s Bank (Dublin) One Guinea

- Early Irish Banknotes: Ffrench’s Bank (Dublin) One Pound

- Type C (Post Bills)

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Five Pounds

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Four Guineas

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Four Pounds

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Three Guineas

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Three Pounds

- Type D – Charles FFrench, Henry Taaffe, Michael Morris, William Keary & Thomas FFrench (1814 only)

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Three Pounds

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Thirty Shillings

- Early Irish Banknotes: Ffrench’s Bank (Dublin) One Guinea

- Type D (Post Bills)

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Three Guineas

- Early Irish Banknotes: Ffrench’s Bank (Dublin) Three Pounds

- Type A – Charles FFrench, Michael Morris & William Keary (1812 only)

- Infamous Irish Banks: Lord ffrench & Co (Tuam & Dublin) 1812-1814

- Carlow Bank (MaCartney, Henry & Co) ?-1813

- Dublin (The British Exchange Bank) 1815-1818

- Dublin (Thomas Finlay, Jnr & Co) 1816-1829

- Dublin (Sir William Barr & Co) 1817-?

- Dublin (George La Touche & Co) 1817-1823

- John David La Touche from 1823

- David La Touche from 1843

- Dublin (Morris, William & Co) 1812-1818

- Cork (Leslie, Charles & Co) 1819-1826

- Cork (Roberts, Sir Walter & Co) 1815-1819

- Cork (Moylan, Denis) c. 1813

- Dublin (Finlay, Thomas) 180?-

- Fermoy (Anderson & Staig) 1816-1821

- Waterford (Hayden & Rivers‘ Bank) 1816-1824

- Waterford (Scott‘s Bank) 1816-1824

It illustrates why self-regulation is even worse than no regulation, and why constant monitoring and strict financial regulation with enforceable penalties is necessary.

- O’Brien Banknote Guide: A Brief Timeline of Irish Banking Failures in the 18th & 19th C

-

1821

The Suspension Period officially ended on 1st May 1821, although it took some time to come into effect. The main benefit of ‘paper money’ was that it gave certainty at a time when much of the copper coinage in circulation was counterfeit and much of the silver coinage was clipped (under-value). In order for a ‘safe’ return to the gold standard, a new coinage was needed.

The British Treasury responded with a new gold ‘one pound’ coin known as a sovereign to compliment the Great Recoinage of George III – started in 1816 and rolled out to all corners of the British Empire thereafter.

- To put a ‘gold standard’ into effect, and avoid the pitfalls of bi-metallism, silver coins were declared legal tender only for sums of money up to £2. This prevented an ‘arbitrage market’ in gold and silver coins from forming.

This sudden burst of silver coin production by the Royal Mint was not matched in Ireland and left the smaller, under-capitalised banks vulnerable to runs on their promissory notes. From 1816 onwards, any monetary shocks (due to failed harvests, trade blockades, etc.) in the banking system were severe. Nevertheless, new banks continued to open all over Ireland and they issued notes to facilitate new business.

- Clonmel & Waterford (Scott, Thomas & Co) 1821-31

- Dublin (Plunkett, Matthew & Co) 1821-1827

- Cork (Newenham, George Jnr. & Co) 1824-1825

-

1826

In 1826, the Irish pound was replaced by the pound sterling and later Irish banknotes were issued denominated in sterling. Thence forward, all transactions in Ireland were in sterling. The Act of Union (1800) was followed by a second (less well known) “union” followed in 1825 – a “customs and monetary” union – the Irish pound was thence tied to sterling and almost “free trade” conditions followed. If the act of 1800 was unpopular, the customs & monetary union was an economic disaster!

- Unable to compete with a rapidly industrialising neighbour, many of Ireland’s proto-industries collapsed and the economy shifted to the export of food and primary commodities such as wool and leather.

- This coincided with the rise (post-1800) and fall (post-1826) of the Irish banking industry

- There was a huge number of small private banks by the year 1800.

- Despite their numbers and their initial success, few managed to acquire sufficient capital to ensure stability

- These small banks were vulnerable in a period of economic change.

- This coincided with the rise (post-1800) and fall (post-1826) of the Irish banking industry

- Dublin (Gibbons & Williams) 1833-1835

Many of Ireland’s early banks depended for their survival on the issue of banknotes. Each denomination had its own serial numbers and every note was signed by the chief cashier. Careful records were kept of issued and returned notes, so that duplicated serial numbers (indicating forgery) would be spotted, and lost or damaged notes could be accounted for.

- The penalty for forging a promissory note was death but this did not seem to deter some

- Bank of Ireland, One Pound, 5 November 1821, contemporary forgery

- Attempted fraud of a National Bank of Ireland (Thurles) trying to claim three payments from two banknotes

In 1845, a period of financial crisis prompted new legislation to regulate the issue of notes. Only six Irish banks were authorised to issue banknotes and this new law allowed notes in ’round pounds’ only, so banks had to withdraw (over time) any of their banknotes in guineas, fractional guineas and such oddities as 25s, 30s and 35s denominations. The ability to print their own banknotes gave these six banks a huge commercial advantage over any new and/or emerging 19th C rivals.

- The Age of the Private Banks in Ireland was over.

- One by one, they either crashed, quietly closed or were taken over by the larger, better capitalised and more stable joint-stock banks

- Their premises and books of business were usually taken over by the bigger banks, so there was some continuity – except for the smaller towns, which were left without a bank and suffered commercially.

We buy current, recent and old banknotes

We buy banknotes from all over the world. This includes Irish, British, European and all countries worldwide. We especially like older (vintage) banknotes but will gladly accept your old holiday change, or accumulations in old wallets, junk boxes and attic clearances. Please note, some countries make their banknotes obsolete every 10 years or so, and these banknotes are no longer legal tender for foreign exchange purposes, e.g. Canada and Switzerland change their banknotes regularly to prevent counterfeiting and tax evasion.

_____________________________________

If you have any queries regarding Irish banknotes, please email us on

old.currency.exchange@gmail.com

____________________________________________________________

If you found this website useful, please connect to me on LinkedIn and endorse some of my skills.

Alternatively, please connect or follow my coin and banknote image gallery on Pinterest.

Or, follow me on Twitter (I post daily)

Thank you

i want to change old bank notes and coins , as i never had a passport , i cant do it at central bank , im irish , i work at the guarda barricks , im living in mayo ,i have a social wlefare card with my picture on it how can i exchange them

LikeLike

You do not need a passport – a drivers licence or social welfare photo ID should suffice.

Just go to the Central bank in Dublin and ask them to lodge the money into your bank a/c if the total is more than €100.

If the total is less than €100, they will exchange your notes and coins for immediate cash.

The new rules were introduced to reduce money laundering, so it doesn’t really affect most people.

The staff at the Central Bank are really nice and they usually go out of their way to be helpful, so don’t worry.

Bring along your Garda ID if you feel it might help but I’m confident it will be a painless process.

Alternatively, you could bring your cash to a dealer.

If your banknotes are in ‘uncirculated’ condition (look like they are new), a dealer will pay more than their face value.

If you scan them and attach to an email, I will let you know if you should go to a dealer.

You can email me at old.currency.exchange.gmail.com

LikeLike