Introduction:

The idea of a separate currency goes back to the sitting of the First Dáil Éireann in 1919 as this newly declared independent parliament declared its intention to govern all 32 counties of Ireland. Many Irish politicians declared that they wanted a completely independent republic – as called for in various speeches in the run up to the 1916 Rising and thereafter.

The reality for the Irish Free State (Saorstát Éireann) when it arrived in 1922, proved to be very different:

- An alternative parliament was declared for Northern Ireland in 1920

- It was fully recognised by Westminster and opened by the king himself

- It was a major stumbling block in the Treaty negotiations

- It existed before the Irish Free State, therefore it could not be ignored

- An Irish Free State of just 26 counties (out of the 32) came into existence in 1922

- It was only begrudgingly recognised by Westminster

- Some MPs were arguing for invasion and taking Ireland back into the UK

- This was a worry for Irish politicians, i.e. how ‘free’ were they?

Financial realities created another set of problems when it finally dawned on politicians on both sides of the Irish Sea that the Irish banks were powerful institutions in their own right and, having provided a currency for Ireland for almost one hundred years, weren’t going to be pushed around by politicians in Dublin or London – or by those in Belfast.

- Six of them printed their own banknotes

- They all had significant numbers of shareholders from London

- They were private companies, i.e. they answered to shareholders, not politicians

- Their banknotes (and the money that backed them) belonged to them

- It was were THEIR money

- It did not belong to the British or Irish state !

- They also paid stamp duty on the their notes

- This was an income stream neither government wanted to lose

- All circulating notes were subject to Stamp Duty of 7 Shillings per £100 (0.35%) p.a.

- The newly formed Irish Free State treaded carefully

- They wanted their own, independent currency

- There was much to do in the meantime, so a new currency was shelved

- They established an Irish Banking Commission in 1925

The Great War (1914-1918) had focused a lot of attention on the idea of money and how safe it really was. Irish Joint-Stock banknotes had been made legal tender in 1914, due to the war situation. The 1914 Act allowed the Irish banks to substitute British currency notes for bullion, as cover for their excess note issues. This arrangement was revoked at the end of 1919 and the notes of the Irish Stock-Banks were no longer legal tender. Bank of England notes were, but they were no longer backed by gold, i.e. Britain did not return to the gold standard after the War. Thus, during the 1920s, the need for a distinctive Irish currency and an authority to control its issue became apparent.

The British government had devolved local government powers to Belfast (in 1920) and Dublin (in 1922), so they didn’t have to do anything. They could afford to sit back and watch… and only intervene if it suited them. They could, in effect, choose their diplomatic battles.

- They wanted to keep Ireland in their empire – as a self-governing dominion

- Tying the Irish Free State to Sterling was a means towards achieving that

- The Currency Commission (1927) when it came, was a ‘slave currency’ to Sterling

The newly formed Northern Ireland government couldn’t do anything

- They were financially dependent on Britain

- They didn’t want to break with Sterling

- They ‘went with the flow’

- The Joint-Stock Banks continue – to this day – to issue their own notes in Northern Ireland

Independence:

Independence, when it finally came in 1922, was a busy time for everyone in the new Dept. of Finance. They had to plan, set budgets, manage expectations and disappoint as few people as possible. With capital rapidly flowing out of the country, this cannot have been an easy task. The Civil War (fought between 1922 and 1923) complicated things.

- The matter of a national currency was put at the bottom of a long list of priorities

- The Irish Free State continued to use British coins and Irish Joint-Stock Bank notes

Banknotes used in Ireland in 1922:

Irish Free State / Saorstát Éireann and Northern Ireland

- Six banks – each with their own banknote designs

- None of these ‘promissory notes’ were a de jure national currency

- The Irish Free State had no Central Bank, so there was no system in place for one

- The notes of the six issuing banks were simply a de facto legal tender… since 1825 !

- That said, if one of these banks failed, their notes were worthless

- The reality was, of course, that these were ‘safe’ banks with sufficient backing

- The Irish Free State sought a more stable (and accountable) national currency

- All six sets of banknotes were used both north and ‘south of the new Irish border’

- From a banking and monetary perspective, it was almost as if nothing happened

1922-28 Joint-Stock Banknotes for Irish Free State & Northern Ireland

The Irish Banking Commission:

An Irish Banking Commission was set up in 1925. Its purpose was to initiate, develop and implement a plan to deliver a national currency. It did deliver but the execution of their plans were not easy, or simple.

- The national currency did not arrive quickly

- A series of iterative steps (a phased plan) was required.

The first challenge was identified quickly, i.e. the Bank of Ireland was set up as a national bank in 1783 but it was reduced to the status of a joint-stock bank by the 1845 Act. Although it was the largest bank in Ireland, with a history of acting as a quasi-central bank, it was a private company and was legally answerable to its shareholders, not the Irish Free State. Further complications were then recognised: the banks operating in Ireland were of very different characters and finding a compromise that was both pragmatic and agreeable would be challenging:

- Issuing Banks (6)

- The Bank of Ireland had been founded under Royal Charter

- It was set up as a national bank, but never achieved full central bank status

- After the Banking Act (1845), it became a joint-stock bank, albeit a very large one

- It was the Irish Government’s banker in the 18th C

- It remained the British Government’s banker in Ireland after 1800

- It carried on as the Irish Free State’s Government’s banker after 1922

- The Provincial Bank had been incorporated in Great Britain, but its head office was in Dublin

- It was a British bank operating solely in Ireland – north and south !

- The National Bank was first registered in Ireland but had its head office in London

- It was a was a London clearing bank

- The Northern Banking Company, the Belfast Bank and the Ulster Bank all had their head offices in Belfast – they were, legally speaking, foreign banks

- The Belfast Bank now operated exclusively in Northern Ireland (from 1923)

- Non-Issuing Banks (4)

- The Royal Bank now operated exclusively in the Irish Free State (from 1923)

- The Hibernian Bank – one of Ireland’s oldest banks – was not a note-issuing bank

- The Munster & Leinster Bank was not a note-issuing bank

- Its head office was in Cork and it operated solely within the Irish Free State

- The National Land Bank – Ireland’s newest bank – was set up by Dáil Éireann in 1919

One source of contention between the British and Irish Free State governments was about how to apportion the Stamp Duty from the six Joint-Stock Banks that were issuing their own notes in Ireland. This was a substantial annual revenue. The British Government wanted to retain it and the Saorstát Government were keen to take it, or at least a major portion of it.

In 1928 they agreed the following:

- Bank of Ireland

- 87% in the Irish Free State / Saorstát Éireann

- 13% in Northern Ireland

- Provincial Bank

- 82% in the Irish Free State / Saorstát Éireann

- 18% in Northern Ireland

- National Bank

- 95% in the Irish Free State / Saorstát Éireann

- 5% in Northern Ireland

- Northern Bank

- 28% in the Irish Free State / Saorstát Éireann

- 72% in Northern Ireland

- Ulster Bank

- 42% in the Irish Free State / Saorstát Éireann

- 58% in Northern Ireland

- Belfast Bank

- 0% in the Irish Free State / Saorstát Éireann

- 100% in Northern Ireland

This thorny issue of stamp duty and apportioning would raise heckles in Dublin, Westminster and Irish banking circles right up until 1928, when the Saorstát Goverment proposed raising stamp duty from 0.35% to 1.5% and this was relevant in terms of how many Ploughman notes each of the five (note-issuing) bank could print in 1929.

The next difficult question was: How to quantify how many notes the Consolidated Banks were allowed to issue? Five of them were already note-issuers and the Bankers (Ireland) Act, 1845, had granted the right to issue notes to the Bank of Ireland, Provincial, National, Ulster, and Northern – all of which exercised this right on an all-Ireland basis. The note issue of these banks was made up of two components—the Fiduciary issue, and the Secured (or non-fiduciary, or excess) issue.

- Each bank was allotted a fiduciary quota by the Bankers (Ireland) Act, 1845.

- The issuing banks could issue banknotes up to that quota figure, without any specific cover, or backing, for the notes, save the “unlimited liability of the banks”

- Worryingly, some of these banks had become limited companies

- Any notes issued over and above the maximum fiduciary issue formed part of the “secured issue”. They were so called because the secured issues had to be protected ‘pound for pound’ by securities deposited with the Bank of England.

- The issuing banks could issue banknotes up to that quota figure, without any specific cover, or backing, for the notes, save the “unlimited liability of the banks”

The Commission was not satisfied with the existing state of affairs, and, in particular, saw some dangers and undesirable features:

- It disliked the note issue monopoly granted to the six banks—only five of which were within the jurisdiction of the Saorstát—and wanted to amend it.

- The profits resulting from the issue of secured notes accrued to the Bank of

England—the agency supplying the backing for the notes. - Under the prevailing conditions, banks without the right of issue had to obtain bank notes from the issuing banks, with consequent profit to the issuers. The Commission felt that it would not be equitable or wise to continue that situation.

The Commissioners reported:

“We are of the opinion that we cannot conscientiously recommend the continuance of the fiduciary privilege upon its present basis”

The Commission recommended that the fiduciary issue be consolidated, and that it be jointly controlled and issued by an independent, non-political central institution to be known as The Currency Commission.

- The Establishing of the Irish Pound: A Backward Glance

- John L. Pratschke (1926)

- Journal of the Institute of Bankers in Ireland, April 1926

The Currency Commission:

The Currency Act 1927 resulted from the Banking Commission’s recommendations.

- The Act provided for the establishment of a Currency Commission as an independent non-political body to control and manage a new Irish currency, the “Saorstát Pound”

- The Currency Commission was granted power to issue the so-called Lady Lavery Notes (or, A Series Legal Tender Notes), in denominations of 10 Shillings, £1, £5, £10, £20, £50, and £100.

- The first issue date of each denomination of these notes was 10-SEP-1928

- They entered circulation on this date of issue

For more information see:

- Link: Currency Act, 1927

- Link: The Currency Commission of Ireland

Banknotes used in Ireland in 1928:

Irish Free State / Saorstát Éireann

The Irish Currency Commission introduced a new national currency in 1928, comprising a new set of banknotes and a new set of coins. The notes were titled in both Irish and English language. The coins were in Irish only.

- Currency Commission (Lavery Notes)

- 10/-, £1, £5, £10, £20, £50 and £100 notes

Currency Commission of Ireland £5, dated 23rd October 1928. Signed by Brennan & McElligott

Meanwhile, the Currency Commission allowed the five note-issuing banks to continue circulating their own banknote designs – until some better arrangement was agreed. That solution was now only a year away, i.e. the Currency Commission of the Irish Free State’s Consolidated Series (the famous Ploughman notes).

Banknotes of 1928:

- Irish Free State:

- Set 1

- Currency Commission – Series A (Lavery)

Lady Lavery Notes – The Old Currency Exchange, Dublin, Ireland

- Set 2

- Joint-Stock Banks – each with their own banknote designs

- Bank of Ireland, National Bank, Northern Bank, Provincial Bank and the Ulster Bank (Same as from 1922 onward – no change)

- Joint-Stock Banks – each with their own banknote designs

- Northern Ireland

- Set 3

- Six Joint-Stock banks – same as above (no change needed)

- Bank of Ireland, Belfast Banking Company, National Bank, Northern Bank, Provincial Bank and the Ulster Bank

- These notes were also acceptable ‘south’ of the Irish border

- Six Joint-Stock banks – same as above (no change needed)

The Consolidated Banks:

The Consolidated Bank Series solved the problem of notes being used on both sides of the Irish border and the constant arguing over how to apportion Stamp Duty. It also greatly simplified the Saorstát banknote designs, i.e. down from 6 different sets of banknotes to two. It did, however, increase the number of Joint-Stock Banks issuing their own banknotes from five up to eight. These eight banks now shared a common design, i.e. the Ploughman series. The only argument now was about how many notes each bank would issue for each denomination.

Banknotes used in Ireland in 1929:

Irish Free State / Saorstát Éireann

- Two sets of banknotes

- Set 1

- Currency Commission (Lavery Notes – same as 1928)

- 10/-, £1, £5, £10, £20, £50 and £100 notes

- Currency Commission (Lavery Notes – same as 1928)

- Set 2

- Consolidated (Ploughman) Notes – 8 banks with a common banknote design

- Bank of Ireland, Hibernian Bank, Munster & Leinster Bank, National Bank, Northern Bank, Provincial Bank, Royal Bank and Ulster Bank

- £1, £5, £10, £20, £50 and £100 notes

- Bank of Ireland, Hibernian Bank, Munster & Leinster Bank, National Bank, Northern Bank, Provincial Bank, Royal Bank and Ulster Bank

- Consolidated (Ploughman) Notes – 8 banks with a common banknote design

One Pound Ploughman Notes – Set of 8 Consolidated Banks + Reverse Design (in centre)

The quotas of Consolidated Bank Notes allotted to the banks under the Currency

Act, 1927, of Saorstát Éireann, were those recommended by the Parker-Willis Commission, with one minor modification.

- Originally, the National Land Bank (formed in 1919 by Dáil Éireann) was to be allotted a quota of £55,000 on the recommendation of the Commission. However, the Bank of Ireland absorbed the National Land Bank in July, 1926, buying the interest of the Minister for Finance in it , for .£203,000.

- As a result, the quotas established by the Act increased that of the Bank of Ireland by £55,000 to £1,760,000 and eliminated the quota of the National Land Bank.

The quotas were as follows:

Quota for each Consolidated Bank.

The actual number of notes issued seems to have greatly exceeded these quotas but the figures are taken over a number of years. Issue numbers for their £20, £50 and £100 notes are unknown. See table below:

Ploughman Notes – Numbers Issued by each Bank

Northern Ireland

The Bankers’ Northern Ireland Bill fixed the provisions for the creation of the Northern Ireland Issue in place of the all-Ireland issue of the six issuing Irish Joint-Stock banks. It became law on 2 July 1928.

- Set 3

- Six banks – each with their own banknote designs. Five of the six banks changed their designs for use in Northern Ireland in 1929 and issued a new series of their notes. They were not supposed to circulate ‘south of the border’ but they were generally acceptable. This, at last, solved the ‘thorny’ Stamp Duty problem.

- Bank of Ireland (First Northern Ireland issue, 1929-1958)

- National Bank (First Northern Ireland issue, 1929-1934)

- Northern Bank (First Northern Ireland issue, 1929)

- Second Northern Ireland issue, 1929-1968)

- Provincial Bank (First Northern Ireland issue, 1929-1944)

- Ulster Bank (First Northern Ireland issue, 1929-1934)

1929 Joint-Stock Banknotes for Northern Ireland

- The Belfast Banking Company had pre-empted this in 1922 by selling all of their branches in the Irish Free State to the Royal Bank of Ireland who, in turn, had sold their branches in Northern Ireland to the Belfast Bank.

- Belfast Bank (First Northern Ireland issue, 1922-1968)

The Central Bank of Ireland:

A second Banking Commission was appointed in November 1934, to consider the situation of banking within the Irish State, including the dual notes in circulation (Lady Lavery + Ploughman notes) and the status of the eight note-issuing Joint-Stock banks then operating within the Irish Free State.

- The most important of its recommendations were:

- A Central Bank with greater powers be established in place of the Currency Commission

- A cessation of the right of note issue for the eight associated banks, i.e. the end of the Consolidated Banknote issues

It published its final report in 1938:

This resulted in a new set of banknotes where the title “Currency Commission of Ireland” was replaced by “Central Bank of Ireland” on all new notes. Thus the Ploughman series of notes was a necessary step in the path towards a recogniseable national currency for Ireland with a single set of coins and banknotes.

See below:

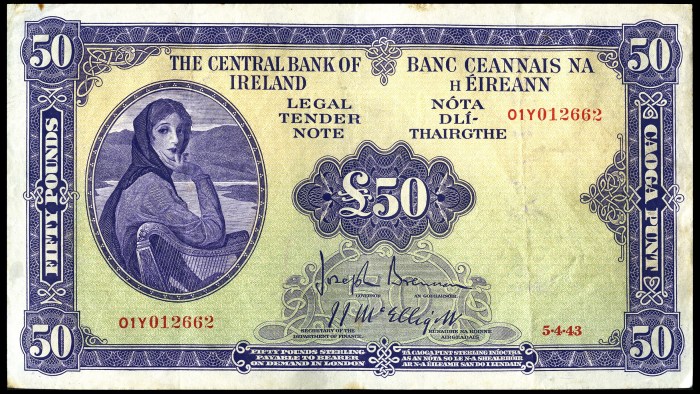

1943 £50 Central Bank of Ireland, 5 April 1943, Brennan-McElligott signatures.

For more information see:

- Link: Central Bank Act, 1942

Of course, this wasn’t the end of this story because the new notes were still printed in Britain by the Bank of England, there was a panel clearly stating that these notes were Sterling notes, with a promise to pay the bearer on demand in London.

This panel was dropped from Irish banknote designs in 1960

Full Monetary Independence:

Ireland would not completely break from Sterling until 15th December 1978, when it was announced that Ireland would participate in the EMS. Countries were given the option of either a 2.25% or 6% margin of fluctuation within the EMS’ Exchange Rate Mechanism (ERM), and Ireland took the narrower margin.

The EMS started on 13 March 1979, and towards the end of the month Sterling started to gain in value against the EMS currencies because of rising oil prices, and by 30 March Sterling breached the upper fluctuation band limit of the Belgian franc and the Irish currency could no longer track Sterling.

- After over 50 years, the parity of the Irish and British currencies was broken

- The Irish currency became known as the Irish pound (or Punt)

- We then issued a second series of banknotes: the B Series

- These B Series notes were printed at Sandyford, Co Dublin

- The last link with the Bank of England had been broken

Further Reading:

- Money and Banking in Ireland (Origins, Development and Future)

- PADRAIG McGOWAN, Central Bank of Ireland (1988)

- Journal of the Statistical and Social Inquiry Society of Ireland. Vol. XXVI, Part I

- A Chronology of Main Developments in the Central Bank of Ireland (1943 – 2013)

- Published by The Central Bank of Ireland (2013)

- Central Bank of Ireland website