Introduction

A currency board is an institutional arrangement for managing a currency with a fixed parity. The currency board is much more constrained than a central bank, insofar as these constraints help ensure that the fixed parity is maintained. The board’s main activity is to issue a local (slave) currency at a fixed rate of exchange against a foreign (master) currency.

- Slave currency notes are issued only against receipt of master currency

- The currency board earns seigniorage by investing the proceeds of note issue in external securities denominated in the master currency

- Those that were operated in former British colonies in Africa and Asia are usually regarded as the classic examples, the West African Currency Board and the Pan-Malayan Currency Commission

- The West African Currency Board included: Nigeria, the Gold Coast (now Ghana), Sierra Leone and The Gambia.

- The British West African pound was also adopted by Liberia in 1907, replacing the Liberian dollar, although it was not served by the West African Currency Board. Liberia changed to the U.S. dollar in 1943.

- Togo and Cameroon adopted the West African currency in 1914 and 1916 respectively when British and French troops took over those colonies from Germany as part of World War I.

- The Pan-Malayan Currency Commission included:

- Straits Settlements

- Penang, Singapore, Malacca, Dinding, Christmas Island, the Cocos Islands and the island of Labuan

- Federated Malay States

- Selangor, Perak, Negeri Sembilan and Pahang

- Unfederated Malay States

- Johor, Kedah, Kelantan, Perlis, and Terengganu)

- Brunei

- Straits Settlements

- The West African Currency Board included: Nigeria, the Gold Coast (now Ghana), Sierra Leone and The Gambia.

Origins of the Irish pound

When the Irish Free State became independent in April 1922, it retained most of the legal structures which it had inherited from its years in the UK. Until March 1979, shortly after the establishment of the European Monetary System in which Ireland, but not the UK, fully participated from the start, Irish currency remained at par with sterling.

From the legal point of view, the period from independence to the establishment of the European Monetary System in 1979 falls into three parts.

- the period of private currency (before 1928)

- the lifetime of the Currency Commission

- the Central Bank of Ireland sterling link period from 1943

As a consequence of the British currency reforms of the mid-1840s, six of the nine Irish joint-stock banks retained currency issuing privileges, although all issues beyond an initial grandfathered sum had to be fully backed by gold, silver (or, during the suspension of convertibility from 1914 to 1920, British currency notes).

Consequently, at independence in 1922, much of the currency in circulation represented the obligations of Irish banks. However, this was in no sense an autonomous currency. All of the banks still operated in Northern Ireland and they were all obliged to hold liquid reserves in London, where two of the largest had their head offices.

- Their notes and other obligations were still payable in British currency

- Continuation of this state of affairs posed no obvious problems to the Irish Free State

It was the introduction in 1926 by the new Government of a series of distinctively Irish token coin that began to raise some doubt or ambiguity about the status of Irish currency. Although the new coinage represented more a gesture of national pride than of economic policy, the concept of an Irish pound became an issue.

In order to address the question, the Government appointed an ad hoc Commission under the chairmanship of H. Parker Willis of Columbia University, New York.

- Four of the other seven members of the Commission were directors of Irish banks.

- Within six weeks of its establishment in 1927 the Commission had issued a report whose recommendations determined the future course of the Irish pound.

The Currency Commission, 1927-1942

The outcome of the Willis Commission’s recommendations was

- The establishment of a new unit of account at par with sterling

- the creation of a standing Currency Commission (1927) to administer the introduction of Irish legal tender currency notes against receipt of sterling – the first notes issued in 1928

- the consolidation of the existing private bank note issue into a single parallel currency, part of the seigniorage on which was taxed

The new unit of account was, by default, the currency of contract within the State. However, it was fixed at a one-for-one parity with sterling and it was also called a pound, i.e. the Saorstát pound, or Free State pound.

- After 1949 when the Irish Free State became the Republic of Ireland, the currency was known simply as the Irish pound

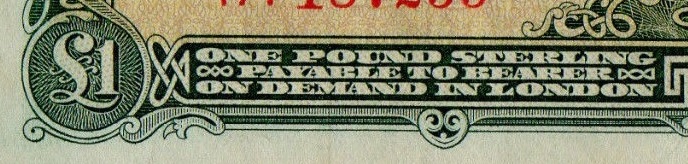

Convertibility was effected through a guarantee that any Irish pound notes would be paid at par (without fee, margin or commission) in sterling at the Bank of England in London, acting as agency for the Currency Commission. This guarantee was printed on a panel on all Irish banknotes up until 1960.

Sterling panel – £1 sterling payable to the bearer on demand in London

The essential financial arrangements of the Currency Commission were those of a currency board, rather than of a central bank. Thus in particular it was not empowered to lend, whether to banks or government. Its notes had the status of legal tender. All notes issued had to be backed 100 per cent by a reserve consisting of gold and sterling balances.

The main banks were shareholders of the new Currency Commission, and they elected three of the seven directors. Three more were appointed by the Minister of Finance and the seventh was elected by these six as a chair. The very substantial role of the private banks partly reflected the conservative financial policies which the Government of the new state had espoused; it also partly echoed the original balance of power in the US Federal Reserve District Banks (Professor Willis had been Director of Research at the Federal Reserve Board).

The adopted model thus embodied what might be regarded as

- a British solution to the question of parity and currency issue

- plus, an American solution to the constitution of the governing Commission.

The next challenge was “what to do with the pre-existing bank notes, issued by Irish banks under British law,” and their solution proved to be a novel one.

Instead of simply arranging for the existing bank notes to be compulsorily retired in favour of the new and untried Currency Commission notes, it was decided to replace them with a consolidated series of notes guaranteed by the banks as well as by the Currency Commission.

These consolidated notes were not legal tender, but each had the private bank of issue’s name clearly printed on it and they proved to be fully acceptable. All of the shareholding banks, including the two that had no previous note-issuing rights, were entitled to issue up to a fixed quantity of the consolidated notes.

The old issues had to be retired, and the size of the total issue of new consolidated notes corresponded more or less to the old issue. An annual fee, which amounted to as much as 3 per cent. (equal to the banks’ own prime lending rate) was payable by the banks.

Thus most, if not all, of the seigniorage on the consolidated notes accrued ultimately to the Government. Not surprisingly therefore, the total issue of consolidated notes never reached the ceiling and they were phased out after 1943, by which stage they accounted for only 22 per cent of Irish notes in circulation, down from 40 per cent in 1934.

The Central Bank of Ireland

Following the report of another ad hoc Government Commission of Inquiry into Banking, Currency and Credit in the 1930s, it was decided to replace the Currency Commission by a central bank with expanded powers. The Central Bank of Ireland began operations in 1943. But its activities were tightly circumscribed by the continued existence of a backing requirement for the currency and by the fact that the banking system, with its large net holdings of external assets, had no need of the new Central Bank as a lender of last resort.

- For the next decade at least, the Central Bank operated as if it had not acquired the new freedoms

- It lent neither to the banks nor to the Government, It made no efforts to influence the trend of credit through regulations or interest rate actions

- Its main policy intervention was an outspoken critique of the “constantly increasing scale of the expenditure of the State and local authorities” contained in the Bank’s 1950-51 Annual Report

- This led to a protracted public controversy and led to the early retirement of the Bank’s Governor

I possess 2 x £5 Currency Commission Ireland Banknotes in reasonable condition.

What are they valued at ??

The dates are 5/7/38 and 23/9/40

LikeLike

These early Irish notes vary greatly in value by condition/grade and by date.

Some dates are extremely valuable as not many survive.

I cannot value anything without seeing it.

LikeLike